The advent of artificial intelligence into various spheres of human activity is rapid and ubiquitous. The banking domain is moving in the wake of the AI-driven revolution, leveraging this technology in multiple use cases. Mortgage lending is one of the shop floor operations in the vertical where AI tools benefit borrowers and creditors alike.

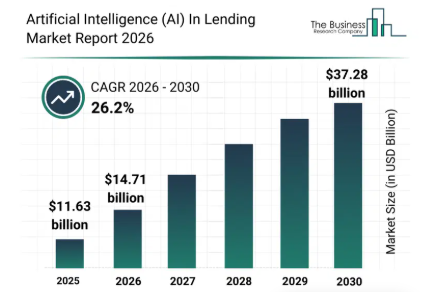

As a 2025 Stratmor Group survey revealed, the percentage of lenders utilizing AI-fueled tools has increased from 15% to 38% in a single year, displaying a solid CAGR of 26.5% and pushing the global AI market size in lending to a breathtaking $14.71 billion in 2026.

Let’s see how artificial intelligence streamlines and facilitates loan pre-approval and final approval – the fundamental validation processes that enable access to money for people who want to buy a home.

Borrower Evaluation: The AI Way

Before a bank or other financial institution agrees to lend a person a certain sum to purchase a house or apartment, it should ensure the person can repay the debt. It is done through underwriting, during which the organization assesses the borrower’s assets, credit story, income, and property value. Until recently, this procedure was entrusted to human personnel, resulting in a rather sluggish, error-prone routine. AI-fueled underwriting significantly improves the efficiency of this workflow.

What are the stages of AI-powered borrower evaluation?

- Automated document processing. Thanks to natural language processing (NLP) and optical character recognition (OCR), artificial intelligence reads and verifies pay stubs, tax returns, bank statements, and other documents that contain data on the potential borrower’s financial condition and solvency.

- Deep risk assessment. After analyzing alternative data (like rental payment history or utility bills) and behavioral patterns regarding spending or debt accumulation, machine learning (ML) models forecast the candidate's employment stability, potential for income growth, and default probability.

- Real-time fraud detection. AI can identify unusual digital footprints, altered documents, or submission anomalies in the applicant's data that indicate fraud.

- Dynamic decisioning. AI algorithms give the green light to low-risk applications but flag more complex or borderline cases to be submitted for human review.

And what is vital: AI tools can complete all these steps more quickly and accurately than human employees. As financial organizations claim, AI-assisted borrower evaluation and mortgage approval proceed from 40% to 90% faster, while the number of errors plummets by 90%. What takes underwriters 3-5 business days is done by machines within a couple of hours. The enhanced consistency, accuracy, and efficiency increase the loan approval rate by 20-30% while reducing default rates by 25%.

Despite the weighty advantages these impressive numbers testify to, the use of AI-driven software for mortgage loan approval has potential downsides for customers.

Zooming in on AI-Related Risks for Mortgage Loan Applicants

Like any other immature technology, artificial intelligence may cause problems during loan approval.

- Inaccuracies and hallucinations. The client data provided by AI tools may be inaccurate or even false. The same is true of the information applicants receive from AI chatbots about loan products, interest rates, or legal requirements.

- Algorithmic bias and misuse of alternative data. Historical data used for training AI algorithms often contains racial, gender, or other kinds of prejudices. Besides, AI software may tap into information about a person’s e-commerce activity or social media behavior that has nothing to do with their creditworthiness. All of these may potentially lead to discriminatory loan approval decisions.

- Lack of transparency. When a loan is denied, AI may fail to provide substantiation of the decision, so the candidate doesn't understand what is wrong with them or what they should correct to reapply.

- Data security and privacy. AI tools process tons of sensitive personal and financial data, such as tax returns, income sources, credit history, employment status, etc. When pooled into a centralized storage, this information is subject to greater leakage or breach risks that may result in identity theft, blackmail, or legal implications for customers.

- Missed context. Acting according to rigid rules, AI often fails to grasp broader context. For instance, the tool will place much store by a one-time income dip that happened due to seasonal or medical reasons, or disregard the specifics of local job markets and deny the loan

Given all these bottlenecks, it is evident that AI-based solutions can’t replace mortgage brokers now or any time soon. High-tech tools improve the overall loan approval pipeline but require constant human oversight by qualified experts who control the use of AI and can understand diverse financial conditions and niceties (for instance, the complex structure of self-employment income) to make a well-considered, balanced loan approval decision.

Luckily, LBC Mortgage has such vetted professionals on its roster. Our specialists offer a wide range of loan products, work across 10 jurisdictions, and have experience collaborating with a broad variety of lenders with unique life stories and financial circumstances. We accompany you throughout the entire customer journey and consider numerous nuances to ensure a satisfying experience of arriving at the destination – owning a residence that reflects your vision of a comfortable, functional, and cozy home to a tee.

Drawing a Bottomline

Artificial intelligence has brought tectonic shifts to workflows in multiple sectors, and the banking and finance industry is no exception. When used for mortgage loan approval, AI-based software helps brokers in borrower evaluation by facilitating document processing, risk assessment, fraud detection, dynamic decisioning, and more. However, personnel should employ AI tools cautiously because their performance often suffers from hallucinations, inaccuracies, algorithmic bias, misuse of alternative data, lack of transparency, questionable data security, and other shortcomings. To ensure the high quality of service and mitigate risks, a top-notch mortgage broker agency should practice a human-in-the-loop approach, prioritizing human oversight of AI's performance and adoption of critical decisions by competent professionals.