Learn the differences between dry and wet funding to choose wisely

Taking a mortgage loan, mind your location — in most US states, a traditional “wet” funding mechanism applies. This is when the loan unlocks as soon as the deal closes and costs become accessible, i.e., liquid, right after the fact.

But while this is the standard case for most US geographies, there are states that allow “dry” funding of your mortgage loan, which are more in favor of lenders. Specifically, dry-funding loans are more legally thorough, ensuring a lender gets full procedural completion before releasing mortgage costs.

But for home buyers, the adjacent scrutiny can be confusing and complicated. Dry funding takes more time, keeping mortgage costs locked after the loan closure and right up until the disbursement of funds.

If it’s your first time buying a home or refinancing a property, figuring out dry funding — where it is allowed, how it happens, and why it’s needed — is essential.

Dry Funding Put Simply

Certain US states allow dry closing of a real estate deal. The property transaction process that follows the dry closing is called dry funding. Here’s how it works:

- Traditional real estate deal closing (followed by wet funding) — you close the loan, and a lender disburses mortgage costs the same day;

- Dry real estate deal closing (followed by dry funding) — you close the loan, and a lender keeps mortgage costs locked in for a bit longer, until more ensuing formalities are completed, then disburses them.

In most states, wet funding is the only and primary mechanism of mortgage funding, which puts forth — mortgage costs turn liquid once you’ve closed the loan, thus the “wet” terminology. The deal closes, and the costs become accessible to a home seller, while the lender finalizes all documents and legal formalities on their side.

In contrast, you don’t get immediate access to funds and property ownership after a dry deal closing — the costs don’t turn liquid until the lender finalizes the documents and legal formalities, thus the “dry” terminology.

What Exactly Happens During Dry Deal Closing?

The prolonged dry closing period is used by a lender to conclude all the paperwork and formal legal necessities. During that time, the property transaction stays incomplete. It remains that way until the lender is all set and all legal conditions are met.

To be exact, the lender takes their time to:

- Sign all loan closing documents: including the mortgage file, deed, disclosures, and settlement paperwork.

- Formalize party agreement: all parties involved provide signatures, formally agreeing to the property transaction terms.

- Review the loan file: the lender may want to verify employment, confirm insurance coverage, review title documents, or check any last-minute changes in the borrower’s financial state.

- (Re)approve loan documents: all the signed documents can be sent back to the lender for approval and revision if need be.

- Provide the final authorization: the lender gives final authorization and only then wires loan funds to the escrow company or closing agent. The costs are disbursed.

After all of the above procedures, the property ownership deed is officially recorded with the local county recorder's office. And only once the funding and recording are complete, property ownership legally transfers to the buyer.

Why is Dry Closing a Thing?

The need for dry property deal closing can be either enforced locally or employed by the lender for some extra legal security and accuracy.

Situations may vary:

- Some state regulations may require funding only after document review.

- The lender may need additional time to verify loan conditions.

- There are title or documentation issues that must be resolved.

- The transaction closes near a weekend or holiday and funds cannot be transferred immediately.

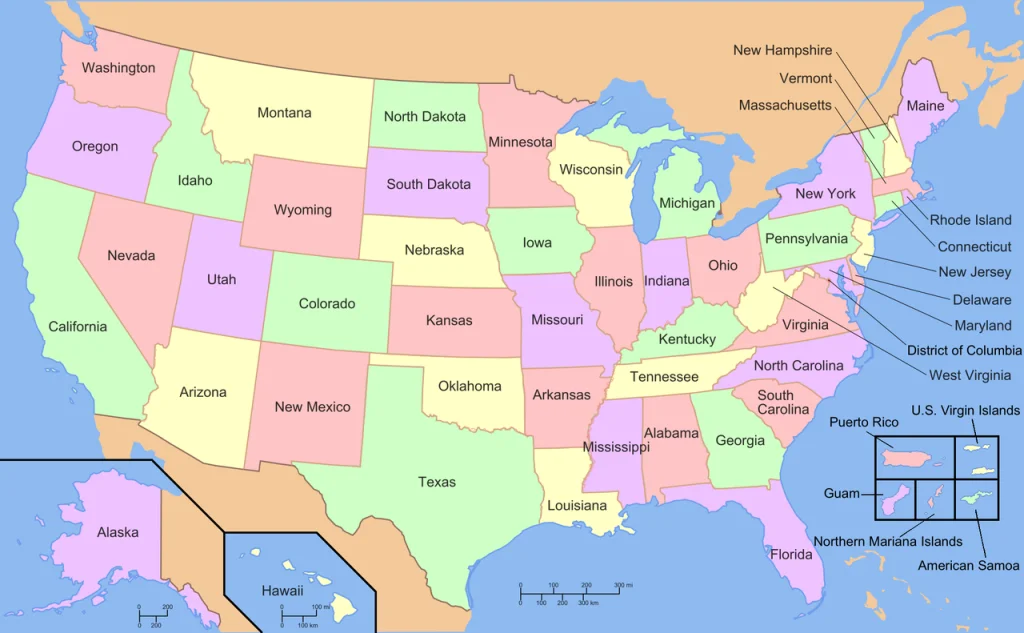

Which States Allow Dry Funding?

Naturally, dry funding is very location-based — not all states have adopted the mechanism. Most regions prefer a straightforward wet process. A bunch of states allow dry deal closing in addition to the normal wet funding procedure. But for the US states, it’s more of an exception than a rule.

Here all dry funding states to date:

- Washington

- California

- Arizona

- Oregon

- Nevada

- New Mexico

- Idaho

- Alaska

- Hawaii

These are all big metro areas, which encourage more lending flexibility and control, through dry funding in particular.

Wet Funding Geography

Wet funding is the procedure of choice for all other states in the US, from Texas and Wyoming all the way to North Carolina and New York. Interestingly, dry funding is more a Western rim thing — if you take a look at the map of states, dry-funding states are situated on the west edge of the country.

Source: Wikipedia

The rest are all wet funding states stretching from the Midwest through Central areas and to the Eastern border. Hawaii and Alaska are the most “exotic” states by far to have adopted the dry funding approach.

Comparing Dry Funding vs Wet Funding

| Point of difference | Wet funding | Dry funding |

| Funds are released | Immediately at loan closing | After lender reviews and approves all loan closing conditions |

| Property ownership is transferred | At the same time funds are disbursed | After all formalities are finalized — funds can be released before the ownership transfer |

| Closing speed | Generally faster transaction completion | Slightly slower due to post-signing verification |

| State availability | Common in most states | Common in Western and some Midwest states, like California and New Mexico |

| Document review process | Completed before closing appointment | Final review frequently happens after signing |

| Risk for lenders | Slightly higher because funds are released immediately upon loan closing | Lower because lender get to verify documents before opening funding |

| Risk for buyers and sellers | Less uncertainty after singing | More waiting time between signing and funding |

| Recording of documents | Usually occurs immediately after funding | Frequently occurs after funding approval |

| Delay between signing and funding | Same day | One to several business days |

| Best for | Straightforward property transaction where are legal requirements are already satisfied | Property transactions that require additional verification, compliance checks, or lender review. |

Which to Choose in Your Case?

Ultimately, if you are getting a mortgage in the state that allows dry funding, you gain more legal flexibility and accuracy at the expense of process delays. Thus:

- Wet funding is for buyers who need a fast closing, sellers who want immediate access to proceeds, and property transactions with fully approved documentation.

- Dry funding is for states that legally require post-signing reviews, complex property transactions (e.g., multi-staged, home equity loans, etc.), loans with additional underwriting conditions, and lenders seeking extra verification compliance for secure release of funds.

How LBC Mortgage Can Help You

Need help securing a property loan? Consult your choice of location, loan options, and best-fitting funding mechanism with experts at LBC Mortgage. We offer a multi-service mortgage and property management platform that will help you automate intimidating mortgage tasks.